🔒 Ethereum Foundation Debuts 'Trillion Dollar Security' Initiative. The initiative aims to map security shortcomings, promote fixes and communicate strengths of the Ethereum network.

🫏 Democrats Ask Treasury to Provide Report on Trump's Crypto Ventures. Democrats in the House are asking for 'suspicious activity reports' on Trump's various crypto efforts.

🇹🇭 Thai Government to Tokenize $150M in Government Bonds. The Thai government is planning an initial offering of 5 billion baht in 'G-token' tokenized government bonds.

📸

Daily Market Snapshot: After briefly pushing above $2,700 yesterday evening, ETH's breakneck rally paused on Wednesday as the rest of the crypto markets big players also shed value.

tl;dr Since 2023, Ethereum has ceded the distribution edge that once turned ETH into money by throttling its own L1, urging builders to “get off mainnet,” and moral‑policing whole product categories, a choice that scattered users, liquidity, and mind‑share across L2s and faster L1s. The result was a broken product‑money feedback loop—apps no longer pulled in users who attracted builders and liquidity—leaving ETH to trade like a discounted tech stock while capital fled elsewhere.

The remedy? A product‑first, L1‑first pivot: increase base‑layer capacity, treat every chain (even roll‑ups) as a competitor to be won, and position Ethereum mainnet as the decentralized economic hub for the coming wave of tokenized assets. With a refactored 2-year roadmap targeting a 10× gas ceiling, an L1 zkEVM, and tighter L1‑L2 integrations, the Ethereum pivot can rekindle the original virtuous cycle, pull builders and traders back to mainnet, and reassert Ethereum’s claim as crypto’s second global money.

The Broken Loop

ETH’s 2021 ascendance happened because ETH was being priced as the second money to emerge out of crypto.

Downstream of the trillions of new post-covid dollars, people realized that money was a myth, and the market was looking for new mythologies to believe in. Bitcoin was obviously one, but in 2021 people realized that a fixed cap wasn't the only way to produce money out of blockchain technology.

In 2021, people identified a positive feedback loop in the Ethereum system, and the output of that loop all pointed towards value capture in ETH the asset.

Apps attracted users, which attracted more builders, which attracted investors. Traders arrived to optimize market efficiencies, and the excesses of all this showed up as protocol revenue.

Positive feedback loops are powerful forces. They make you wince when a microphone picks up its own signal. They are the runaway energy explosion of an atom bomb. They are the lockdowns during a global pandemic. Strong positive feedback loops are unignorable, even to the indifferent person.

The market saw the strength of Ethereum’s positive feedback loop, and it priced ETH accordingly. We had a good thing going!

What Happened?

If you hear the crescendoing screech of a microphone picking up its own signal, how do you stop it? You simply sever the connection between the speaker's output, and the microphone's input. You cut the feedback loop, and stop it from growing.

This is exactly what Ethereum did, when it placed Rollups too early in its roadmap.

Ethereum’s strength originally came from the L1 being the obvious place for builders to get their first users, for users to be able to access the apps they desired, and for speculators and traders to make everything run smoothly. If you wanted to build in crypto, you went to the Ethereum L1.

There was no second best.

As the rollup-centric-roadmap came into view, official messaging from Ethereum leadership, and unofficial messaging from the Ethereum community, placed L2s as the centerpiece of Ethereum’s future. “Ethereum is scaling with L2s” was chanted across the ecosystem.

The costs of this were not fully appreciated at the time. Builders suddenly had to pick a winner among a dozen rollups; users wondered where their friends (and liquidity) would migrate; exchanges and wallets scrambled to keep up. What was imagined to be competitive-cooperation between Ethereum’s L2s manifested as zero-sum unproductive infighting.

Before rollups, getting Ethereum exposure was easy: just buy ETH. But, since Ethereum was relying on its rollups for its next phase of growth, exposure to this growth required a basket of rollup tokens, and opinionated speculation on winners or losers. How could ETH possibly be money in this context?

With the Schelling point of the L1 gone, the strength of Ethereum’s signal dissipated.

The market stopped pricing ETH as a crypto-money, and started pricing it as a tech-stock with a discounted cash flow (DCF) model.

This is not good, since no L1 crypto-asset looks good under a DCF model. ETH stopped looking cheap compared to Bitcoin, and started looking overvalued compared to other L1 smart contract ecosystems with higher growth rates in their ecosystems.

Ethereum went from being uniquely dominant in its category, to being viewed as sharing the same category as a number of other smaller, faster, more centralized competitors.

The difference between Ethereum holding 90% versus 60% market dominance is a huge difference. The former is a global internet currency, while the latter is a tech platform.

It took a while for this to show up in the ETH price, but we all know the story of ETHBTC and the relative weakness ETH has shown in the last 3 years. Despite the 3-day, $700 increase in ETH in May 8-10, ETH is still down 72% versus Bitcoin and down 84% versus Solana over the last 900 days.

Some might say that the relative ETH weakness is due to exogenous factors that should not be an indictment of any strategic failure in Ethereum.

Michael Saylor has poured $35B into Bitcoin over the last 3 years.

Solana memecoins have locked up hundreds of millions of dollars of SOL in LP contracts.

Both of these are examples of capital that could have been won by the Ethereum ecosystem, but were instead ceded to other options.

No Michael Saylor for Ethereum could emerge while there’s a broken feedback loop between Ethereum’s economy and its assets. The context doesn’t support it. The decision to allocate capital to BTC or MSTR is an easier choice when there is no second-best crypto asset.

Memecoins on Solana are a more complex beast. Ethereum will never support the 400ms blocktimes that encouraged the memecoin economy on Solana. Nonetheless, the rise of Solana’s developer ecosystem and general supportiveness to applications attracted the builders that Ethereum pushed away after 2022.

Ethereum’s Pivot

Ethereum is a decentralized ecosystem. There is no central intelligence in Ethereum – signals emerge from the margin, and the correct signals get stronger over time. By 2024, the correct signals had found the correct ears, and changes started to be made.

My podcast with Ansgar and Dankrad from the EF was a discussion about this process, and the concrete specific changes that had been made in Ethereum leadership to account for strategic missteps taken in Ethereum from 2021-2024.

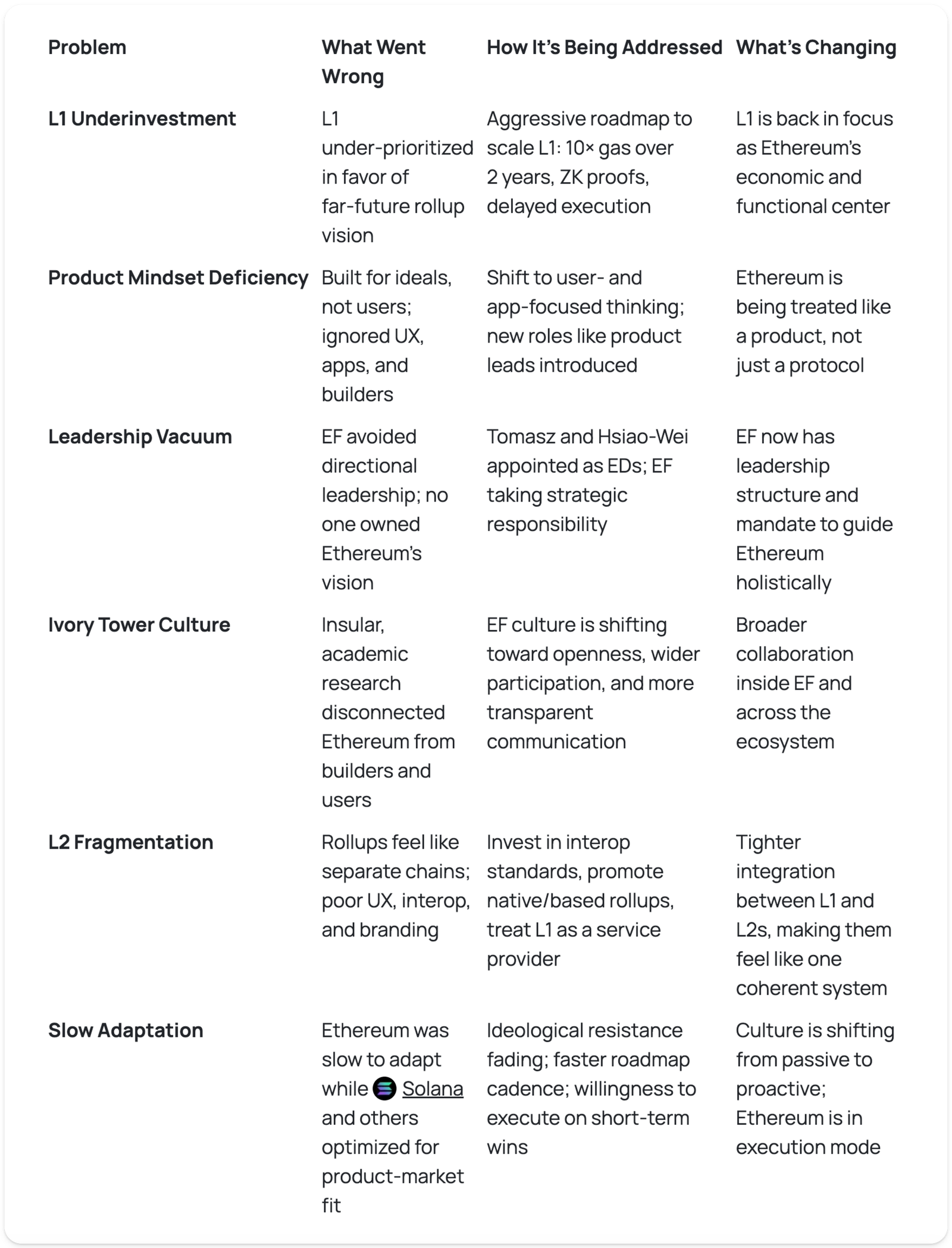

I made a cheat sheet of all the categories of malaise in Ethereum, and the concrete steps being taken to remedy the issues:

There is a debate in Ethereum about whether this was a ‘pivot’ or a ‘reprioritization’. I’m not sure it matters – it's semantics. What does matter is the level of priority that Ethereum has for its ecosystem components.

It is critical that Ethereum prioritize itself first, before it prioritizes L2s. The Ethereum L1 must be the highest priority for the Ethereum ecosystem – Ethereum’s L2s should not lead the Ethereum roadmap, and especially not ahead of the needs of the L1. This is the cart leading the horse.

Ethereum’s priorities:

L1 technical capacity + strength

L1 App ecosystem + user base

L2 Interop standards

A weak L1 is bad for everything in the Ethereum ecosystem. It’s bad for users, bad for apps, bad for traders, and bad for L2s. Everything in Ethereum benefits from an increased focus on the strength of the L1.

For the good of the ecosystem, the L1 needs to compete at the highest of levels.

If Ethereum wants to best serve its users, apps, and rollups, it needs to put itself first.

The Ethereum L1 is the Economic Hub of Crypto

The Ethereum L1 should be the default for anyone who wants to build, use, or trade onchain.

It is the only truly decentralized, multi‑client network with perfect uptime. Ethereum is where cypherpunk values can reach everyday users. The mandate should be to extend this incredible foundation as far as possible.

We need to restore the Ethereum L1 as the schelling-point it was always meant to be.

This means scaling the L1 to be the largest tent possible, so that ordinary users, not just whales, can transact while preserving the censorship‑resistant core that gives the chain its value in the first place. Declaring “the L1 is only for the top 0.1%” does nothing but kneecap Ethereum’s appeal.

The correct signal is: Ethereum is home — for developers, for users, and for assets.

Distribution is king. Every breakout moment in crypto, from the 2017 ICO boom to DeFi Summer in 2020 and the NFT wave of 2021, happened on Ethereum because the audience was already here.

In 2024 Solana won the memecoin mania by offering faster, cheaper block space and captured that distribution edge. Ethereum cannot afford to concede that ground again. Scaling the L1 restores the network effects that pull apps and rollups into its gravity well.

At their core, blockchains are asset ledgers. Ethereum is the best ledger available, and it should aim to host the deepest liquidity, the highest volumes, and the tightest spreads. Scaling the L1 expands execution capacity, drawing in traders, market makers, and token issuers who want the biggest, most liquid venue. TradFi is shopping around right now to see where they should deploy their RWAs.

There should be no second best to Ethereum.

The world improves 100x when you accept they're all separate chains.

You: • No longer get baited by Samani • Understand the dynamics at play and why scaling *does* help value accrual

Ethereum needs to act in its own interest and understand ~all others will do the same. https://t.co/QulpaUySC1

L2s are best understood as paying customers of Ethereum. Each L2 controls its own governance, can fork at will, and is free to settle on another chain. Ethereum needs to treat them like customers they could lose, not an integrated part of Ethereum’s tech stack.

The confusion over whether these rollups “are Ethereum” hinges on perspective: if you define Ethereum strictly as the L1 blockchain, then Base, Arbitrum, and friends are plainly independent chains; if you define Ethereum as a broader security ecosystem, they qualify as family because they anchor their proofs to mainnet. Whenever we talk about Ethereum, we need to be clear about which lens we’re using, because the grand “ecosystem” narrative only resonates with people already bought into Ethereum’s long‑term vision, while everyone else simply sees competitive settlement providers.

The concept of a positive-feedback loop across the Ethereum ecosystem – one through which excesses flowed into ETH – is not new. Both of these 3+ year old graphics illustrate that same concept.

The critical error we made is not understanding that each individual L2 has to build this same network effect feedback loop for itself, and without Ethereum having the technology ready to strongly integrate its own L2s, the network effects of Ethereum L2s could not be recaptured by the L1.

Ethereum built L2s before it built interoperability technology. Based + Native rollups, and interop standards came in 2024, 3 years after Ethereum’s first L2s started fragmenting its network effects.

Moving forward, we should prioritize highly integrated Based and Native rollups over independent L2s.

The Ethereum community is part of its product

Ethereum isn’t just software; it’s also the people behind it. As core devs push a product‑driven roadmap, the community carries equal weight—builders choose a chain and its culture together.

That makes us co‑creators, not sideline critics, responsible for driving Ethereum’s visibility and adoption.

We, as the Ethereum community, should own-up the fact that we have not been the most compelling community to join. We have become the ‘Holier-than-Thou’ ecosystem, and we have driven unnecessary wedges between us and much of the ecosystem.

Everyone is midcurving why ETH’s price performance has sucked

Ethereum leadership and culture have alienated users and builders by being hostile to its own app layer.

We publicly exorcised @LidoFinance. We’ve shunned traders and degens.

Many in Ethereum downplay memecoins, partly due to distaste for speculation, partly to avoid legitimizing Solana, and partly because of the grift they can enable, which they see as a distraction from crypto’s core mission.

I did this. Bankless was a leader in setting this tone and messaging. We helped draw the lines that grew into the schisms that we see today – schisms that I am now trying to repair.

It would be one thing if Ethereum simply rejected memecoins. But over time, rejection itself has become part of Ethereum’s cultural identity. What began as a pushback against grift has evolved into a broader tendency to gatekeep what is seen as legitimate.

Much of this stems from the trauma of 2021-2022 (Terra, 3AC, FTX) when fraud defined the era, and Ethereum was largely buffered from the collapse of crypto. The Ethereum “Holier-Than-Thouists” were proven right, but those who were hurt by the fraud nonetheless did not join the ecosystem that kicked them when they were down. They felt rejected.

In a moment when many thought Solana was dead, traders and speculators stayed around. Partly because Solana was a technically superior product for what traders and speculators wanted, but also because the Ethereum community had always shunned traders and speculation.

At the downfall of FTX, had Ethereum chosen to prioritize L1 scaling and been more appreciative of the value that traders and speculators bring, then it would have likely been that Ethereum would have won its third market cycle in a row.

A Holier-than-Thou Ethereum culture persists to this day, albeit we are now licking our wounds from rejecting the participants that are obviously critical to every ecosystem.

Ethereum Cannot Gerrymander its Support

I think Alon got this right:

traders are easily the most important user group in crypto – not creators, not devs

if traders don't see value, creators & devs don't eat and go elsewhere

so if you're tokenizing anything, traders come first

Traders and speculators are the most important user group in crypto. They deposit the first dollars, price the risk no one else will touch, and broadcast clear market signals that pull in builders and users. When Ethereum moral‑polices what counts as a “valid” use‑case, ideologically-indifferent users simply take their liquidity elsewhere.

You might think that developers are the most important user group in crypto, but if traders don’t like what the developer is building, then the developer goes hungry.

The Ethereum community needs to see itself as a part of the Ethereum product suite. Application teams choose a chain partly for its culture. If they sense they’ll have to fight upstream against a community that sneers at “degenerate speculation,” they will pick friendlier waters.

The Ethereum community cannot gerrymander its support around use cases that we believe are morally upstanding, versus ones we find distasteful. We need to take a founder mindset, and optimize for the maximum possible TAM.

If Ethereum wants to remain the hub where assets launch and ideas compound, its culture must be as open as its code.

The Ethereum community has always elevated the significance of its ‘social layer’ as a key differentiator as to why Ethereum is different, unique, and valuable. This ‘social layer’ fixation drove a wedge between people who were ideologically aligned with the Ethereum project, and end users who just want to do things onchain.

Economically rational but ideologically indifferent users were castigated for a lack of sufficient protocol alignment.

Ultimately, all that is truly required of a social layer is selecting the ‘right’ fork, when the consensus code fails. All other applications of the social layer are extra, and should proceed with caution. When it comes to permissionless behavior on permissionless chains, Ethereum needs to walk the walk. This is what credible neutrality looks like.

Fixing the Loop

Ethereum’s great realignment is underway. Maslow’s Hierarchy of Blockchain Development is being restored, this time with the correct order of operations. Ethereum has some incredible assets on its balance sheet – it’s now (imo) in the hands of Tomasz to wire this feedback loop back together, so the strength of Ethereum’s assets – its developers, apps, users, and rollup ecosystem – will once again feedback into each other, and the crescendo of that signal emerging as the increased price of ETH.

Once this happens, the strong-minded ETH-maxis will finally have the strong product foundation they need to stand on to compete toe-to-toe with the Michael Saylors of the world.

ETH as money can only work on top of a strong Ethereum product.

ETH’s path to money has always been on top of Ethereum’s socio-techno product stack. With a successful product realignment, ETH’s can look for higher heights than $10,000.

There is much work to be done to get here, and we must not rest on our laurels. We are at the very beginning of this process. There is still plenty of realigning that must be done across the Ethereum ecosystem.

The Fraxtal ecosystem is expanding at lightning speed—this month’s biggest highlight is IQAI.com, the newest Agent Tokenization platform from IQ and Frax. IQ is building autonomous, intelligent, tokenized agents launching on Fraxtal in Q1. Empower on-chain agents with built-in wallets, tokenized ownership, and decentralized governance—all within a fast-growing Fraxtal ecosystem.

Not financial or tax advice. Bankless content is strictly educational and is not investment advice or a solicitation to buy or sell any assets or to make any financial decisions. This newsletter is not tax advice. Talk to your accountant. Do your own research.

Disclosure. From time to time, we may add links in this newsletter to products we use. We may receive a commission if you make a purchase through one of these links. Additionally, the Bankless team holds crypto assets.