Housing affordability remains historically bleak for everyday Americans thanks to a combination of high home prices, elevated mortgage rates, and limited housing supply.

The outlook for fewer interest rate cuts from the Federal Reserve suggests not much will change in the year ahead.

The average 30-year fixed-rate mortgage hit 6.85% in the week to Wednesday, according to Freddie Mac data.

That’s higher than where it stood a year ago, and more than double what homebuyers could secure in 2022.

Notably, rates on the most popular homeloan have surged since policymakers began the cutting cycle in September.

While the Fed’s benchmark borrowing has dropped 100 basis points in three months, mortgage rates have climbed almost a full percentage point.

To be clear, mortgage rates do not automatically fall when interest rates come down. Like long-term Treasury yields, that figure fluctuates largely based on investors’ expectations about economic conditions and growth.

Mortgage rates are seen falling to 6.34% by the end of 2025, according to 14 models tracked by the real estate research and news outlet ResiClub.

“If mortgage rates fall more than that, it's likely because the labor market weakened more than expected,” said Lance Lambert, CEO and co-founder of ResiClub. “If mortgage rates are higher than that forecast, it's likely the labor market proved more resilient than expected.”

Meanwhile, Zillow reports the average US home value is up 2.5% from a year ago to $357,469.

Nick Gerli, the chief executive of real estate data firm Reventure, highlighted in the chart below that buying a home has only been this challenging twice before in recent history.

Currently, purchasing the typical home requires 39.4% of the median household income — a figure sandwiched between the 38.1% seen in 2006 and the 47.5% seen in 1981, when mortgage rates hovered at 18%.

Housing affordability in 2025

With many economists and forecasters expecting the Fed to hold interest rates steady through much of next year, housing affordability is unlikely to ease that much anytime soon.

In Lambert’s view, two items stand out that could make homes more affordable.

“First being a scenario where the U.S. labor market weakens and a recession occurs, thus pulling down mortgage rates,” Lambert said.

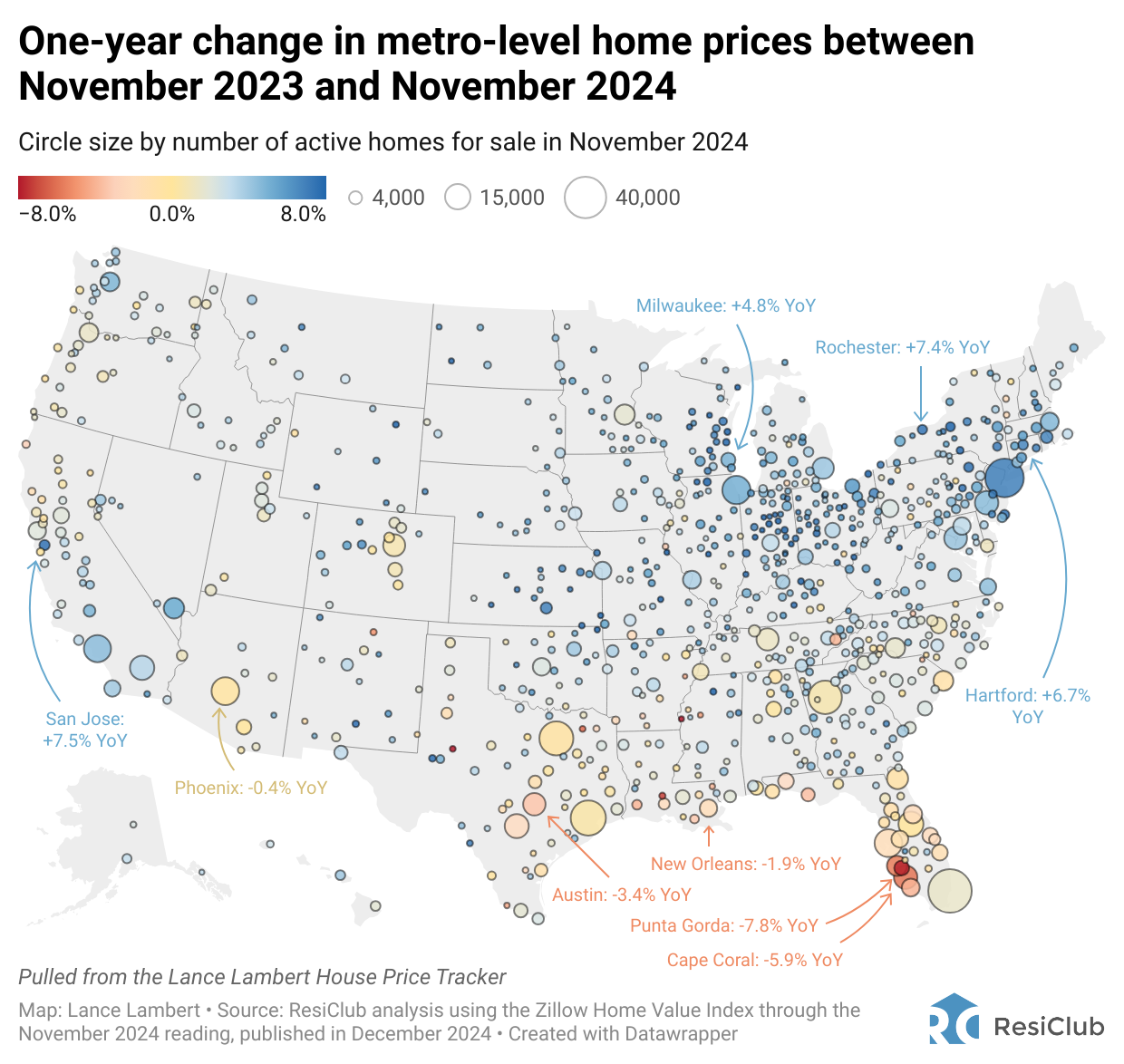

“The second being a scenario where housing market weakness spreads beyond pockets of the Gulf and Mountain West and pushes down home prices in more regional markets. As of today, most markets in the Northeast and Midwest remain tight, with home prices rising.”

Comments or feedback? Reply directly to this email or let me know on X @philrosenn.

Elsewhere:

📊Lots of Americans took on holiday debt this year. A new LendingTree survey found 36% of consumers took on debt this season, with average balances of $1,181. Fewer than half of the people who took on debt expected to do so. (CNBC)

💰️ TheMega Millions jackpot hit $1.15 billion. After no winners were announced Christmas Eve, the massive winnings have ballooned above $1 billion for just the seventh time ever. It’s been three months since a Houston resident claimed the last jackpot of $810 million. (CNN)

Traders see 92% odds the Fed keeps rates unchanged in January, according to Kalshi, the biggest US prediction market: